INTRODUCTION

Managers of manufacturing companies for to meet the requirements of external reporting regarding product costs for stock valuation it’s necessary to approach an invetory-costing method. There are two methods about inventory-costing, namely: absorption costing and variable costing. The choice of such a method by managers is important because it has effects on reportes income, on the evaluation of a manager’s performance, and on pricing decisions. In this essay I will try to define these two methods, to identify the fundamental feature that distinguishes variable costing from absorption costing; to give some arguments for each of them, to explain differences in profit under absorption costing and variable costing, and their use in external and internal reporting.

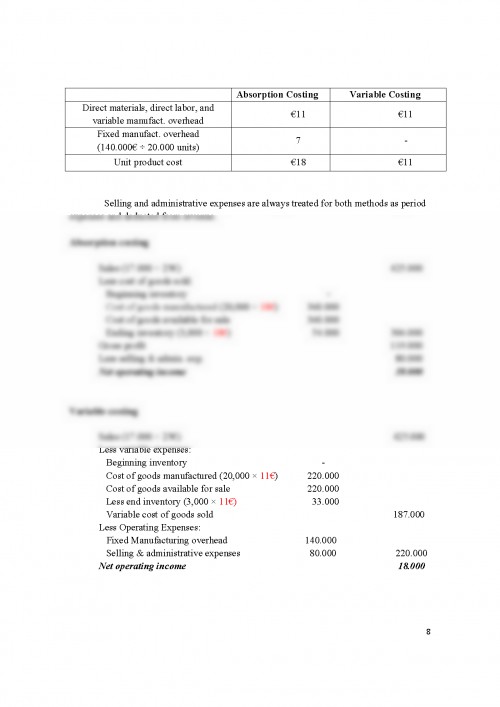

In a manufacturing company, the product (manufactoring) costs are often called inventoriable costs, because they are initially recorded as inventory (as unexpired costs), and after the goods are sold, these become expenses. And also nonmanufactoring costs are called period costs, because they are not allocated to the product and they are recorded directly in income statements. Another aspect worth mentioning is that manufacturing overhead are subclassified into variable and fixed categories.

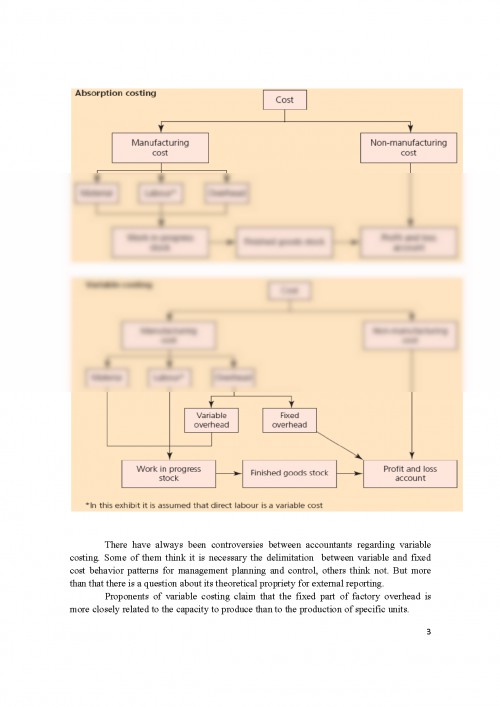

The main difference between the two stock costing methods is that under absorption costing all manufacturing costs are considerated product costs, and they are included in the inventoriable costs, regardless they are fixed or variable; while in the vabiable costing method the fixed manufacturing cost is not included in this category. This last method including in inventoriable costs only direct material, direct labor and variable manufacturing overhead. The fixed manufacuring overhead costs are considerated a period costs, because they are incurred in order to have the capacity to produce. Moreover, they will be incurred regardless of whether anything is actually produced.

Regarding nonmanufactoring costs, both methods are agreed that these costs represents periods costs, excluding marketing and administration costs from inventory.

In the next figure we can notice the different treatment of fixed manufacturing overhead for both absorption and variable costing systems.

There have always been controversies between accountants regarding variable costing. Some of them think it is necessary the delimitation between variable and fixed cost behavior patterns for management planning and control, others think not. But more than that there is a question about its theoretical propriety for external reporting.

Proponents of variable costing claim that the fixed part of factory overhead is more closely related to the capacity to produce than to the production of specific units.

Opponents of this method maintain that inventories should carry a fixed-cost component, because both variable and fixed cost are necessary to produce goods, therefore, both these costs should be inventoriable, regardless of their difference in behavior patterns. There are several arguments for each method which the proponents claim them. Here are some of them.

Some arguments is support of variable costing

a) Variable costing provides more useful information for decision- making.

Managers have to make a lot of important decisions, and all these decision must be based on some accurate information. Thus, a separation of fixed and variable costs is better to provide relevant information about coststs for making decisions. The estimation of costs for different activities requieres a good analysis of cost which will be available only with a variable costing system. Therefore, by adopting this system costing system managers can project future costs and revenues for different activity levels. And this costing system helps the managers to use the best relevant cost techniques for decision-making. Thus this method offers an analysis more evidenced than in absorption costing system.

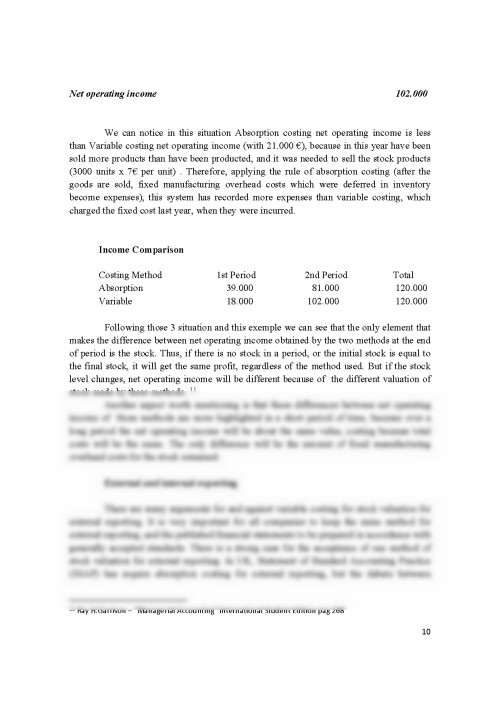

b) Variable costing removes from profit the effect of stock changes

In variable costing case profit depends of sales volume, whereas in absorption costing profit depends of sales and production. Thus, using absorption costing is also possible for profit to decline when sales volumes increase. For exemple if profit is calculated on a absorption basis and stock level fluctuate significantly, this will affect the amount of fixed overheads and therefore profit will be distorted. This situation happens more often for shorter periods of time, for exemple when profits are measured monthly or quarterly. Thus, when the managers want to masure profit at frequent intervals this is the best costing method for them to obtain accurate information about profit. Therefore, these internal profit statements may be used for measuring managerial performance.

Pentru a descărca acest document,

trebuie să te autentifici in contul tău.